")

")

UK ad spend has fallen sharply for the third quarter in a row as marketers grapple with Covid-19 restrictions, Brexit and economic uncertainty, according to new data.

The latest Bellwether report from the Institute of Practitioners in Advertising (IPA)In the three months to October, UK ad budgets were reduced drastically, representing the second-biggest decline since records began.

The record-breaking erosion of UK marketing budgets slowed in Q3 of 2020, according to the latest figures from the IPA Bellwether Report, although a -23.3% fall in spend on advertising is still predicted for the year as a whole.

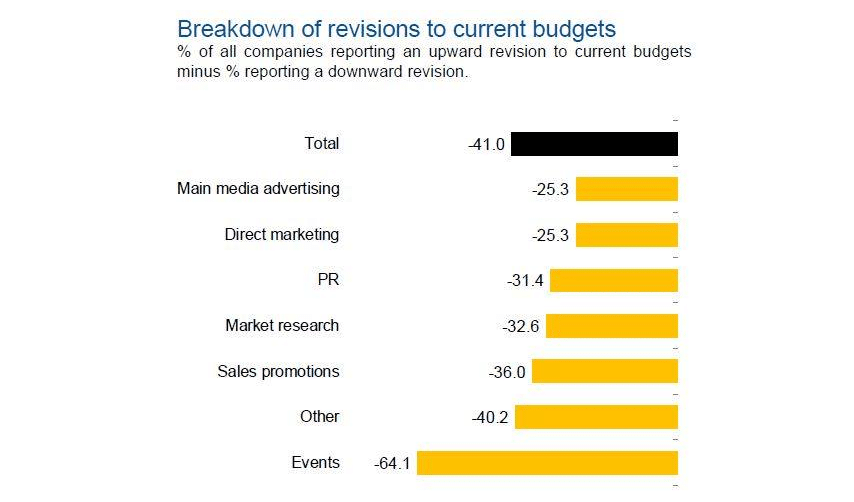

The Q3 2020 IPA Bellwether Report indicates that a net balance of -41% of panellists saw their marketing budgets cut in the third quarter (up from -50.7% in Q2). The result represents the second-quickest decline since the survey’s inception in 2000, only superseded by the reduction in the second quarter of this year.

In Q3, over half of respondents (52.6%) recorded a decrease in budgets from three months ago, compared to only 11.6% that saw an increase.

When explaining falling marketing budgets panellists cited reduced revenues as a result of the COVID-19 crisis, and the need to cut costs in order to maintain profitability.

Ongoing social distancing measures meant that many firms were still operating below full capacity in the third quarter, particularly some services companies that rely on face-to-face client engagement.

Faced with reduced cashflow, businesses reported lower budgets in each of the seven monitored marketing categories. Direct marketing and main media advertising however saw the softest budget cuts with -25.3% of firms recording downward revisions in both categories, compared with -41.6% and -51.1% respectively in Q2.

Underlying data for the main media category signalled that funds available for ‘other online’ campaigns (-6.5% from -35.1% in Q2) were the least affected of the five sub-categories. This was followed by video (-16.1% from 39.3% in Q2), audio (-32.0% from 50.0% in Q2), published brands (-38.5% from 49.2% in Q2) and out of home (-50.0% from 61.2% in Q2) respectively.

Events remained the hardest hit type of advertising, with a net balance of -64.1% of firms registering downward revisions compared to last quarter (up from -76.6% in Q2). Overall, just 3.8% of panellists saw an increase in available spend for events, while over two-thirds (67.9%) recorded a decline.

Looking forward, Bellwether author, IHS Markit still anticipates a robust recovery in economic conditions during 2021, as firms continue to adapt to a ‘new normal’.

This would translate to a +4.6% expansion in GDP and a Bellwether forecast of a +11.3% rise in adspending, followed by a steady trend towards long-term growth rates.

These outcomes, however, hinge largely on positive outcomes regarding the evolution of the pandemic and the development of Brexit negotiations before the end of the transition period at the end of this year.

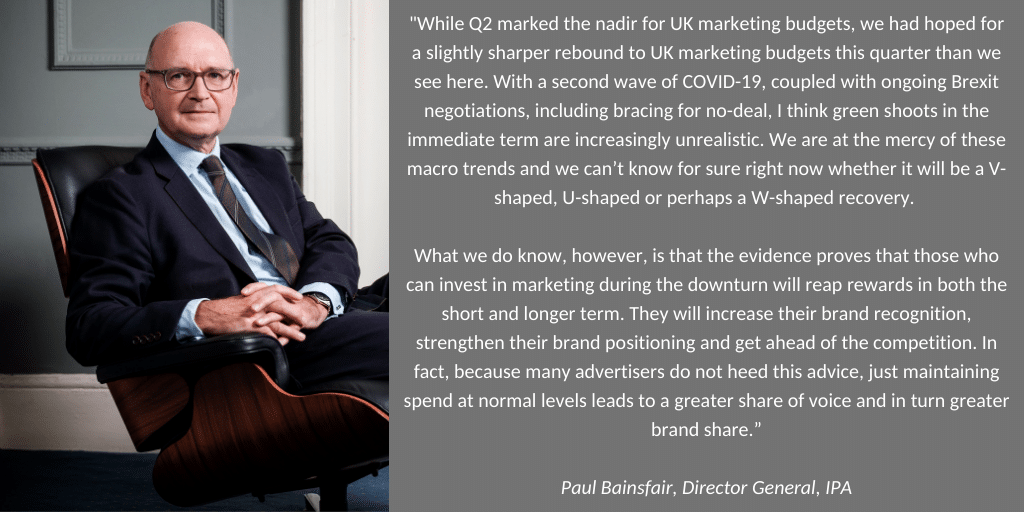

Paul Bainsfair, IPA director general said: “While Q2 marked the nadir for UK marketing budgets, we had hoped for a slightly sharper rebound this quarter than we see here. With a second wave of COVID-19, coupled with ongoing Brexit negotiations, including bracing for no-deal, I think green shoots in the immediate term are increasingly unrealistic. We are at the mercy of these macro trends and we can’t know for sure right now whether it will be a V-shaped, U-shaped or perhaps a W-shaped recovery.

“What we do know, however, is that the evidence proves that those who can invest in marketing during the downturn will reap rewards in both the short and longer term. They will increase their brand recognition, strengthen their brand positioning and get ahead of the competition. In fact, because many advertisers do not heed this advice, just maintaining spend at normal levels leads to a greater share of voice and in turn greater brand share.”

“Smooth EU exit needed”

Eliot Kerr, Economist at IHS Markit and author of the Bellwether Report,said: “With UK businesses continuing to adjust to a ‘new normal’ amid the coronavirus pandemic, marketing budgets remained under severe pressure in the third quarter of 2020. The broad-based decline across all types of marketing budgets highlights the negative impact that the public health crisis is continuing to have on business conditions. Unsurprisingly, events remained the hardest-hit category, with social distancing measures limiting the viability of such spending, although reductions in every other monitored area were also substantial. Looking forward, if the UK can avoid another large-scale coronavirus outbreak and achieve a smooth exit from the European Union, we should see an improvement in economic conditions as firms learn how to better operate in this new business environment.”

“Budget flexibility rather than reduction”

Michelle Wright, MD, Gough Bailey Wright and IPA Chair for England & Wales, said: “The latest report reflects the turbulent period we are experiencing as a result of COVID-19, with marketing budgets continuing their decline, albeit at a slower rate than earlier in the pandemic. Ad spend has reduced across all platforms which is understandable. As the virus continues to disrupt markets, it is important for all businesses to consider their local situation and the likely impact it will face. Reducing marketing spend during a downturn is known to be a risky strategy and ultimately stunts future growth, so brands revising their marketing budget should act with caution and remain flexible.”

The No Deal threat looms

Valerie Ludlow, CEO, ASG & Partners and IPA Chair for Northern Ireland, said: “As we entered Q3 clients restarted previously abandoned projects or asked that we replan their campaign approach to ensure it would withstand a second lockdown (should it be required). We hope this reignited desire to commit to marketing spend is the beginning of recovery for the industry in NI, but I am cautious right now.

“COVID-19 has shown the strengths and weaknesses that devolved decision making across the four regions can bring. The exit from the EU is also looming, and recent news to prepare for a no-deal scenario will have especially challenging consequences for Northern Ireland. As a Regional Head, I am hoping that any negative consequences from both these issues can be avoided to allow our local industry to start on the road to recovery and growth in 2021.”

“Cashflow is king”

Mark Howley, COO at Publicis Media and Interim Chair of the IPA Media Futures Group, said: “The report is broadly in line with expectations. There are two known-knowns of downturns; cashflow is King, and we can see 39% of companies reported a reduction in main media budgets with an eye to cashflow. But equally, there is never a better time to win new customers and build market share, advertising is at its most elastic in downturns. 14% of companies surveyed are seeing opportunity and spending more on main media. The other pandemic effect is the accelerated shift to digital customers, for the average business one-in-five customers were digital at the end of 2109, this is now one-in-three. This shift is reflected in the relative buoyancy of online media spend.”

Industry comment

Ali MacCallum, CEO UK of leading out-of-home agency Kinetic Worldwide, said: “With uncertainty hanging over every business area, new restrictions being introduced on a weekly basis and short-term nervousness, advertisers have understandably decreased their marketing budgets as reported by the IPA Bellwether report. OOH media has taken less of a hit than in Q2 as it has been used innovatively and intelligently by brands and public bodies as we emerged from full lockdown. As we move towards 2021, brands will require flexibility and instant data analysis as marketing decisions are increasingly short term. Thanks to the digitalisation of posters, automated and programmatic OOH allows for trading and targeting to be delivered across thousands of screens in near real time. Marketers have the option to optimise the OOH creative at a moment’s notice by monitoring sales performance and audience indexing. This amounts to a revolution in the sector as data about news, weather, events, and location can be added to the digital mix to better target consumers.The advertising industry needs to offer more flexibility to brands because we’re facing new level of uncertainties every day – from a possible second Covid wave to Brexit at the end of the year. I believe that we will recover strongly in 2021 as we learn how to navigate this new environment, but until then we need to take the opportunity to innovate how we’re using channels and make use – as much as is possible – of contextually useful OOH.”

Neil Collard, Managing Director of Great State, said: “The reality of a second wave of Covid-19 has – predictably – led to a further downwards revision of marketing budgets into Q3. However, our own research during lockdown predicts that there is a significant shift to developing digital products and services, therefore we have constructed 3 archetypes of businesses: Sustaining risers are a small group but they are needing to invest in loyalty initiatives to retain the customers that they have gained through the last 6 months. Supply gappers represent most business and we have observed that in this space digital products and services have leapt in prominence and importance in board tables across the land. As customers have moved to the digital channels there is increased scrutiny on the value and security of those products. This is translating into increased investment of the function and security of these products and services as they become ever more business critical. It would be easy to hypothesise that these investments are funded by a reduction in marketing budgets. Decline battlers are facing bigger more strategic challenges. These are businesses that are late in the game are realising that their long-term survival may well depend on their ability to develop new digital products and services at pace and so again we are seeing a shift in focus into the digital product area – not only for short term gain but also investing in the capacity and capability of their teams. While uncertainty is definitely the key term until the end of this year, data and insights are crucial to succeeding, as brands need to offer improved digital experiences for people, who have increased and altered their device usage whilst being at home.”

Azlan Raj, Chief Marketing Officer EMEA of data-driven, technology-enabled performance marketing agency Merkle, said: “The record reduction in budgets, and recurrent Covid-19 lockdown restrictions have left the industry low on both confidence and optimism. Just 3 in 10 of respondents are feeling more optimistic about their own companies’ financial prospects than in Q2, and there’s a very real risk that low confidence could itself become a self-fulfilling prophecy of stagnant growth or further retrenched budgets. The green shoots may not feel ‘immediate’, but there are opportunities to get ahead of the curve and back to growth. As we try and get back to normal, consumers are still very much unsettled by what’s going on in the world, and not just Covid-19, but the US election and Brexit too. Brands that can truly support their customers to navigate safely through the stormy waters of 2020, have much to gain. So we’d expect to see a shift in ‘pay and spray’ approaches to advertising, and a greater investment in digital, data and customer experience. The number of touchpoints is still growing, as what customers consider ‘ads’ diminishes, so both into Winter and beyond into 2021, we anticipate that kneejerk digital transformation caused by the Coronavirus will need to mature into strategically-driven, experience-led investment.”

Shazia Ginai, CEO UK of neuromarketing and neuroanalytics company NeuroInsight, said: “It is disappointing – although not unexpected – to see further drastic reductions to marketing budgets. Our research shows that in this emotional time, people are looking to brands to help them understand and frame this difficult experience. As Covid-19 has brought sharp focus to the more fundamental foundations of Maslow’s Hierarchy of Needs such as shelter and safety, customers are likely to be less aware of peripheral brands and brand activity and focus instead on brands that bring either utility or enhanced experiences to their lives. So, there’s a clear opportunity to build more fundamental connections with customers for those that get it right. Additionally, now more than ever, as we face existential threats, people expect brands to weigh in on key issues that affect the world we live in. Brand Purpose may have been loosely tolerated when things were going well in consumers’ lives, but brands need to put their money where their mouth (or brain) is if they’re promising action, or they won’t be easily forgive and may be easily forgotten. It’s heartening that the report predicts a more optimistic outlook for 2021 but for brands, this will only be possible if they can manage – even in these difficult business conditions – to connect to the hearts and minds of their customers. Brands will be remembered if they get it right, and it will position them well on the way to getting back to growth in 2020/1.”

James Patterson, VP Client Services at The Trade Desk, said: “To be truly resilient to the decline of ad spend, which doesn’t come as a surprise given it’s been a turbulent year for the industry, marketers must smarten up fast on the value of digital channels and make sure that every pound spent works as hard as possible. The need for adaptable and effective campaigns has never been greater and marketers are being afforded the perfect opportunity to better understand the flexibility and value of data-driven advertising. Getting the most out of tight budgets is about savvy prioritisation of spend, which is why, at The Trade Desk, we’ve seen investment in Connected TV boom this year, as more marketers use the channel as part of their omni-channel ad campaigns. Looking ahead to 2021, the industry is moving towards a robust recovery. In the meantime, industry professionals must remain nimble and continue to plan ad spend strategically, strengthening their brands’ share of voice by embracing the power of digital.”

Mark Inskip, CEO UK & Ireland, Kantar (Media Division), said: “With the end of the pandemic still out of sight, businesses are continuing to keep costs under close scrutiny. This quarter’s IPA bellwether report demonstrates that marketing budgets are still seeing the brunt of cost-cutting, albeit with slightly less severity than in Q2. This is despite ample evidence that in times of economic uncertainty, brands that maintain visibility, reap the rewards in share of voice and consumer engagement.

“According to Kantar’s COVID-19 Barometer, UK consumers still have an appetite for ads, with only 15% wanting to see significantly less advertising during this time. Clearly, consumers don’t want brands to disappear. It’s no surprise that, until businesses can see the light at the end of the tunnel, spend must be carefully managed, but chopping ad spend too harshly is unwise.

“Instead, smart businesses will maximise ROI by carefully measuring each step of their campaigns, to ensure valuable and engaging content is appropriately targeted and delivered with flexibility. Brands who stay present in consumers’ minds through these tough times, will be well placed to benefit when – as forecast by this report – spend begins to lift again in 2021.”

Martin Vinter, Managing Director, Media at Ebiquity, said: “With the continued challenges presented by COVID-19 and the associated societal restrictions, it is no surprise that the advertising and media market continues to observe profoundly suppressed investment levels.

“While the downward trend is being bucked, recovery is going to be even more prolonged than some expected. The uncertainty continues to weigh heavy on the industry, as it does on all industries. Advertisers will need to focus on a “recovery strategy” that considers the distinctiveness of each medium – even more so than before. Audiences and eyeballs are holding up generally for TV and digital – even increasing in some areas – but, naturally, it is a different story for areas like OOH and cinema.

“Reaching relevant audiences is getting harder – especially the ever fickle 16-34’s. Hence, pathing a road to recovery should focus on short term as well as long term metrics. Impacting brand and direct metrics in the current environment requires the full media planning toolbox. The craft of media planning, as well as a focus on media analytics and effectiveness are the three key factors in the path to recovery for advertisers.”

Patrick Johnson, CEO, Hybrid Theory, said: “2020 has been hard on businesses to say the least. Marketing teams across industries are under more pressure than ever to ensure their efforts in media-buy, targeting audiences and improving campaign performance are efficient and sophisticated.

“By looking beyond the doom and gloom there is actually an opportunity for brands. The final quarter of the year is the lead up to Christmas and a peak time for consumer online shopping. Businesses that adapt and respond to the increased online purchase behaviour and with marketing that reaches both new and existing audiences, will be in good position for the year to come. It’s important to remember that consumer spending hasn’t shut down, some digitally focused business actually saw an increase during 2020. So it’s up to marketers to attract those that are spending with smart insights and connect them with their brands, seizing the opportunity.”

Craig Tuck, Chief Revenue Officer, The Ozone Project, said:“While lacking in surprises, the latest Bellwether Report is certainly reflective of a sector, like many others, that remains challenged and shrouded in uncertainty. While Q2 called for quick advertiser action, the budget revisions seen in Q3 appear much more considered – like a pause for breath as advertisers take the opportunity to re-evaluate and recalibrate.

While the pandemic has undoubtedly been the primary driver of these downward revisions, we continue positive conversations with our customers; be it about programmatic transparency, the power of first party data or delivering better business outcomes.

The longer term forecast of a robust recovery in 2021 is a welcome sign, and we’re cautiously optimistic as we move into the final quarter of this year. Amidst the uncertainty, Christmas will still happen on the 25th December and I’m sure we’re all aligned in hoping that the tills jingle as much as the bells this year.”

Anthony Botibol, VP of marketing at BlueVenn, said: “Robust economic recovery has been predicted for the New Year, but it’s imperative that marketers understand and implement the necessary steps to get there. As furlough schemes end and 2021 budgets start to be considered, organisations have the difficult task of striking the right balance between marketing budgets and other resource needs. Businesses now need to be more strategic, looking inwards at existing customers to understand how to best serve and engage loyal groups. An organisation’s customer database, and the knowledge within, is the one thing that its competitors cannot touch. Focusing on lifetime value and ways to increase strategies to cross-sell or upsell amongst an existing customer base is one way savvy marketers can replace the lost revenue from a reduced new customer pool.

The report suggests that the rate of adoption for programmatic advertising will decrease as we head in the New Year. As an industry, marketing is plagued by issues around ad spend wastage already. The problem lies in identifying where this wastage is occurring, due to lack of transparency in results and the inability to optimise effectively. Therefore, while ad budgets continue to undergo heavy scrutiny and digital advertising becomes more problematic, it’s paramount that brands review their advertising strategy and think about how they can better use first party data and invest in their systems to optimise their cross-channel marketing strategies.”

Sean Feast, Director and Co-owner of Gravity Global, said: “The statistics of course reflect our own experiences in relation to PR, with some businesses either reducing their overall spend or stopping PR altogether. But the figures do not perhaps tell the whole story. There are also many examples of businesses that have, in fact, increased their spend in recent months and not only among the challenger brands (where you might expect it) but also within major corporates. Spend is very much dependent on the sectors in which your clients operate, and for every loser there is more often than not a winner, and a winner happy to invest. New business volumes have also increased substantially, so any reports that the industry is dead on its feet are a little wide of the mark!”

Patrick Reid, Group CEO, Imagination, said: “Whilst it is no surprise that the events industry continues to feel the shockwaves of the pandemic, it has clearly shown the opportunity for experiences to reach outside of the communications’ silo of marketing, beyond the stunts and spectaculars that have become the playbook of comms-driven experiential, and into product and proposition. We anticipate an eventual positive recovery, and already see more brands leaning on businesses like ours to help design valuable new customer experiences. Ultimately this approach leads to an increase in the lifetime value of current customers and underpinning next-generation products, services and business models that will be built on the new consumer behaviours and expectations that emerge in the years to come.”

David Fletcher, Chief Data Officer, Wavemaker UK, said: “With almost all ventures now looking to dig in for a longer haul, then it comes as no surprise that research investments are carrying their share of any decline. As with all crises, COVID should present an opportunity for research practitioners to innovate and reinvent to help advertisers best navigate choppy waters now and better drive growth as recovery inevitably follows. If nothing else, the near daily presentation of data on regional COVID trends – including some excellent visualisations – should inspire all researchers to look again at the importance of data story-telling.”