")

")

Digital ad spend in the UK grew at its fastest rate for nine years during 2016, driven by advertisers’ need to tap into people’s rising use of mobile to watch content, according to new research. The data, from the Internet Advertising Bureau UK / PwC Digital, found that overall ad spend in the UK was […]

Digital ad spend in the UK grew at its fastest rate for nine years during 2016, driven by advertisers’ need to tap into people’s rising use of mobile to watch content, according to new research.

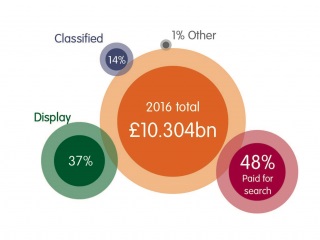

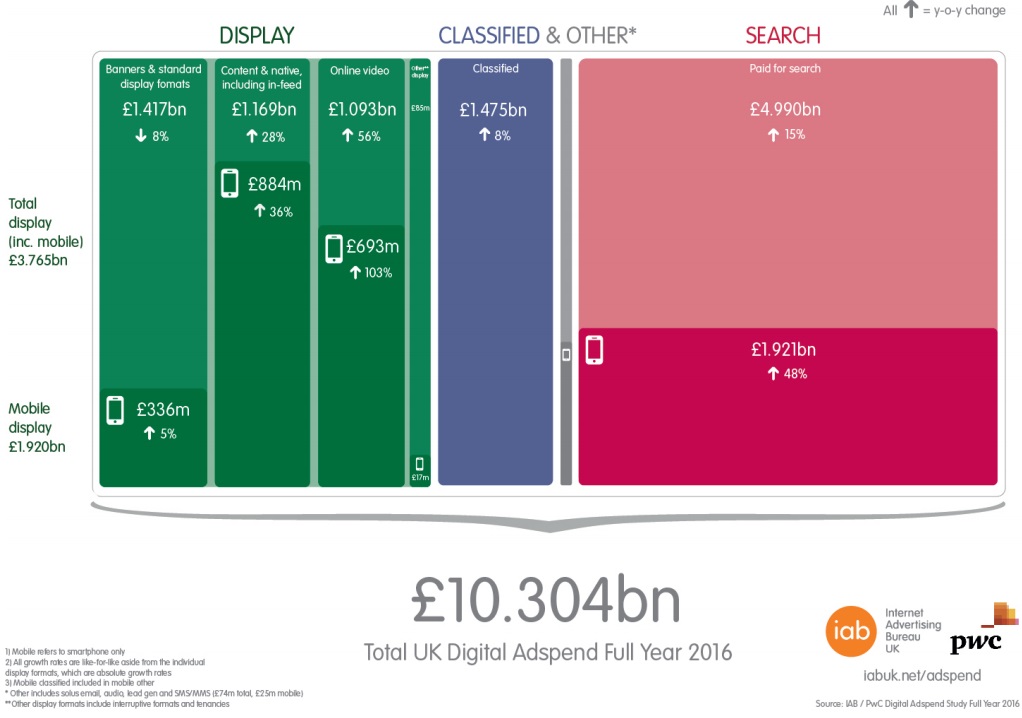

The data, from the Internet Advertising Bureau UK / PwC Digital, found that overall ad spend in the UK was up by 17.3% to £10.3bn over 2016. The last time annual growth was higher was 2007 (38%).

Key findings:

• Digital Adspend grew to £10.3 billion in 2016, up 17.3% on a like for like basis

• Mobile now accounts for over half of all display advertising

• Video was the fastest growing format at 56% on a like-for-like basis since 2015

• Social media display grew 38% to £1.7 billion

The IAB also showed digital in context, with growth outstripping all other UK sectors.

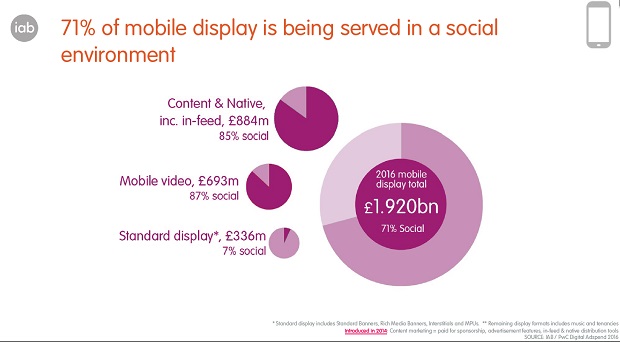

As almost half (48%) of UK internet time is now spent on smartphones, mobile ad spend rose 50.8% to £3.87bn.

Mobile now accounts for 38% of all digital ad spend, up from 4% just five years ago. However, it accounts for 63% of video spend, 76% of Content & Native (including social media news feeds) and 79% of social media spend.

Mobile video is fastest-growing ad format

Spend on mobile video ads more than doubled (up 103%) to £693 million – making it the fastest growing ad format. It accounts for 29% of the total growth in digital ad spend.

The rise in mobile video ad budgets reflects online YouGov data showing that in the last six months, 54% of British smartphone users watched video clips on their phone, with two-in-five of these saying they do more of this than a year ago. A significant number have also watched TV programmes (17%) and films (11%) on their smartphones.

This behaviour is much more prevalent among 18-24 year olds, with 75% watching short clips, 44% watching TV and 33% watching films on mobiles. Six-in-10 people who watched short clips, TV or Film on their phone did so whilst ‘out and about.’

The rise in people consuming mobile and video content has accelerated digital’s growth rate to its highest level for nearly a decade,” said the IAB UK’s Chief Marketing Officer, James Chandler. “Reaching the £10 billion threshold has been made possible by brands breaking the mould, trying innovative formats and making the most of video to reach and amaze people. It’s impossible to ignore the issues the industry is facing at the moment, but digital never stands still and these figures are testament to the long term strength and power of digital.”

Video across mobile and %s is growing at 56%, driven by outstream/social in-feed’s huge 234% rise to £465 million. Outstream accounts for 43% of all video spend but 56% of mobile video. Pre- and post-roll video ad spend grew 12% to £603 million (55% share of all video).

Sebastien Bardin, Sony Mobile’s European senior digital marketing manager, added: “Online video is becoming a bigger priority, providing an impactful and cost-effective incremental reach. In particular, outstream video is great for engaging with our target audience in premium, trusted and viewable environments without disrupting their media consumption or being too intrusive.”

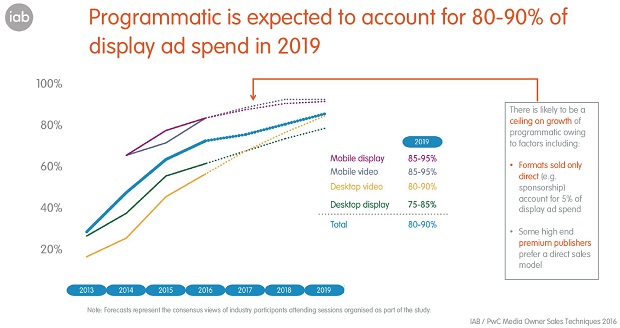

Nearly three-quarters of display is traded programmatically

Display ad spend rose 26% year-on-year to £3.77bn in 2016 – 72% of which was traded programmatically (£2.71bn) – with significant growth coming from direct deals and private marketplaces.

“The biggest change in how display ads are sold is the rise of programmatic direct, which now accounts for nearly half of sales,” says Dan Bunyan, Senior Manager at PwC. “Right now, considerations such as brand safety mean the advertiser is rightly demanding more certainty in the placement of their ads and the industry is evolving quickly to find new solutions to address brands’ needs in this dynamic environment”

Ad spend on social media sites grew 38% to £1.73bn, accounting for nearly half (46%) of display. Social media spend on mobile alone grew 54%. Content & Native ad spend – which includes ‘advertorials’ and ads in social media news feeds – increased 28% to £1.17bn (31% of display).

Search and classifieds

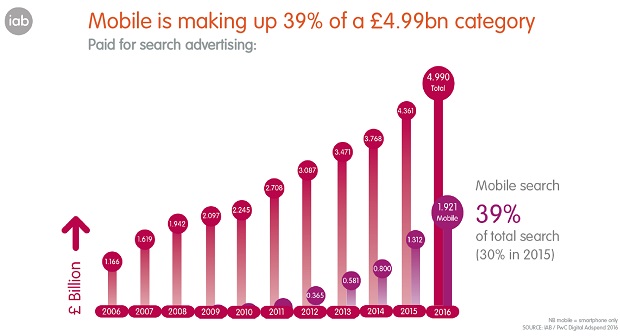

Driven by mobile, which grew 48%, paid-for search overall grew 15% to £4.99bn – a 48% share of digital ad spend. Classifieds, including recruitment, property and automotive listings, grew 8% to £1.48bn (14% share).

The overall picture

The IAB produced this summary of the UK ad spend landscape, illustrating how paid search still dominates, but mobile is becoming a bigger part of that category.

Methodology

The IAB has measured the size of the digital advertising market in the UK in conjunction with PricewaterhouseCoopers (PwC) since 1997.

UK media owners submit digital advertising revenue figures confidentially to PwC who then analyse the submissions and produce aggregated data that shows the size of the UK digital advertising market. Any gaps in the data are filled by the work of the Digital Adspend Advisory Board, which includes the major agency groups, and provides estimated figures for any major media owners that do not submit figures directly to the study.

In addition to figures for the total market, the results show the value of digital advertising by type of advertisement – e.g. display, search and classified and advertising format – e.g. banners, pre-roll video and content / native distribution.

It’s also possible to use the results to identify long-term trend data and to establish the market share of digital advertising in the UK market by using the results with the WARC / Advertising Association figures for other media.

The IAB / PwC Digital Adspend study has now reached its 20th birthday and to celebrate we have created this short video explaining exactly what Adspend is. Check it out below:

View the full report here (registration required).